Weekly Climate Recap: Exxon and Reports Galore

Exxon makes a big announcement on their energy strategy with their foray into lithium. Followed by 2 reports, one from Breakthrough Energy and the other from the US government that highlight the state of the transition through different lenses. Enjoy!

🛢️ Exxon Plays Both Sides

Remember a few weeks ago when I discussed Exxon’s acquisition of Pioneer Natural Resources? In my view of the transaction, I thought this was a clear sign of Exxon’s bullishness on fossil fuel resources. While I still believe that to be true, an announcement this week makes me think Exxon just simply wants to play both sides! Exxon announced that they will be drilling their first lithium well in Arkansas and has the aim to become a leading supplier of lithium for electric vehicles by 2030.

Branded as, “Mobil Lithium”, Exxon’s foray into production of lithium is quite the announcement. Earlier this year, Exxon announced the acquisition of the rights to 120,000 acres of land in Southern Arkansas which is considered be Exxon, “one of the most prolific lithium resources of its type in North America.” This initiative by Exxon has some serious weight behind it with the goal of first production targeted for 2027.

Reading into this announcement coupled with the acquisition of Pioneer Natural Resources, it is my view that Exxon is not an oil supermajor anymore but rather is on the path to become an energy supermajor. Yes, engaging in the energy transition but at the same time capitalizing on demand for fossil fuels.

Further, Exxon’s strategy here is to get in early in domestic production. Currently in the US there exists only one commercial-scale lithium production operation in Nevada with a heavy reliance on imports from Argentina and Chile.

Takeaway: This acquisition is incredibly interesting to me as Exxon shifts to all things energy as opposed to fossil fuels. Different from Shell and BP that have focused on renewables, Exxon appears to be concentrating on other aspects of the energy transition such as carbon capture, hydrogen, and biofuels. All things considered, this acquisition points to Exxon’s transition to energy vs pure fossil fuels.

💸 State of the Transition 2023

Breakthrough Energy has released their State of the Transition 2023 report discussing where we are at in our transition journey. Breakthrough Energy for the unacquainted is a Bill Gates founded organization that focuses on innovating sustainable energy and other technologies to reduce emissions.

“When I founded Breakthrough Energy in 2015, very few people seemed to be talking about how R&D might address the changing climate.” … ”Eight years later, I am no longer asking that question. The climate innovation landscape has changed completely. It’s not an exaggeration to say that we’re in the beginning stages of a Clean Industrial Revolution.”

This was included in Bill gates’ foreword to the report and I feel it accurately summarizes the takeaways from the report, innovation is booming. Interestingly, Breakthrough Energy highlights three key areas that they are focusing on:

⚗️ Hydrogen: Expected to play a key role in decarbonizing certain industries, and seasonal energy storage to fulfill supply and demand matching.

🏭 Carbon Capture: removing historic emissions it important to address climate change, engineered carbon removal and nature-based solutions are options.

🔌 Electrify Everything: Replace as much infrastructure as possible with electric alternative, power grids are a major barrier to this.

The five great challenges in the report are the sectors of our society that together account for all emissions. The key takeaways from each of these challenges and the emissions composition are included below:

(1) Electricity — 29% of emissions

- The world will need 3x the electricity that we consume today by 2050, with this increased demand we need mays to store it efficiently and affordably

- Fusion nuclear may take too long, the strongest baseload power option is fission nuclear

- Electricity grids require a major overhaul and expansion, permitting, siting, and NIMBYism are hurdles to be overcome

(2) Manufacturing — 29% of emissions

- Cement and steel account for 10% of GHG emissions alone but relative to the volume used they are quite efficient

- Abating these emissions should focus on improvements to the supply chain and processing

- Incentivize clean steel/cement through public procurement, tax credits, demo project funding, and other methods

(3) Agriculture — 20% of emissions

- Food demand will increase, we need to be more efficient at fertilizing, raising livestock, conserving water, and reducing food waste

- Methane from cows and livestock is the dominant agricultural contributor to emissions (side note: if only there was an easy solution…)

- Challenges in this sector are highly geographically dependent but it is clear more public R&D funding is needed

(4) Transportation — 15% of emissions

- Encouragingly, the EV problems are as cheap and can travel as far as regular cars

- Raw materials are a major constraint in both supply and geographic accessibility with lithium, cobalt, nickel concentrated in a few key areas

- Long-distance and heavy duty transportation is the biggest technological hurdle, investments are needed to encourage uptake of batteries and e-fuels

(5) Buildings — 7% of emissions

- Existing buildings need to be retrofitted and electrified to make them more efficient

- A/C demand will grow rapidly, heat pump and efficient A/C unit adoption needs to be encouraged

- Behavioural changes are key, the green premiums here are lower than other sectors, all we need is buy in

Takeaway: A lot of words in this story with few images, apologies. I thought this report was interesting to gain a perspective about what Breakthrough Energy is focused on, but more valuable was the diagnosis of the problem among the 5 sectors. Overall, the focus on carbon capture / hydrogen gives me a binary view, either Breakthrough is looking so far into the future that the usefulness of these technologies actually holds water, or, they are taking a view on the transition contrary to my own.

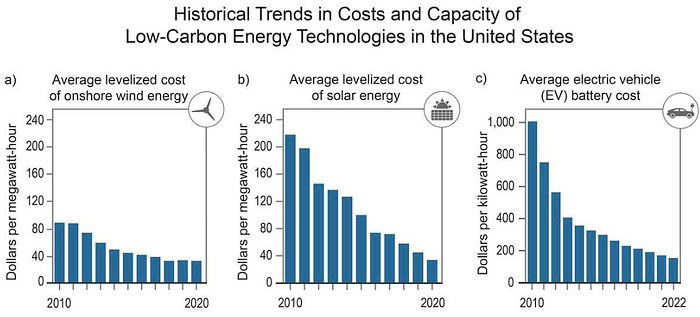

⛈️ US Releases Fifth National Climate Assessment

Headline: Annual US emissions fell 12% between 2005 and 2019 with emissions declining from their peak in 2007. That is the takeaway from the Fifth National Climate Assessment Report. The causes of this decline in emissions:

- coal use declining, natural gas and renewables increasing, in tandem creating a 40% drop in emissions from the electricity sector

- wind and solar costs have declined by 70% and 90% respectively over the last decade

- 80% of new generation capacity in 2020 came fom renewable sources

The US is becoming more efficient at turning energy into economic growth relative to emissions with emissions decreasing while the economy and population have grown.

One area that the report brings light to is the adaptation actions undertaken by different states. Climate action has increased in every region of the US with efforts to adapt to climate change and reduce GHGs being underway in every US region and expanded since 2018. However, the report reaches a conclusion that despite the increase in adaptation actions across the US, the current efforts are insufficient to reduce today’s climate related risks.

Takeaway: While there is some positives that can be gleaned from this report, the reality is that there is currently not enough action being undertaken. While US GHGs are on the decline, the current rate of decline is insufficient to meet the climate commitments at a national and international level. To reach these commitments, the GHG emissions would need to decline by ~6% a year on average, far more than the current average of 1% per year from 2005 to 2019.

What Else is in the News

- “A tax-break scam that has ensnared venture capitalists at the behest of keeping fossil fuel companies in business.” is Michael Barnard’s definition of direct air capture (DAC) technology as noted in his piece here. The article dives into 2 similar sounding companies, Heirloom, a carbon capture company, and Airloom, an innovative wind energy company. This article is worth a read to sense check yourself and understand that not every VC backed company actually has good ideas.

- If you like diverging trends you’ll love to hear that Blackrock just invested US$550m in Oxy Petroleum’s first large-scale DAC plant, Stratos as announced here. The investment will cover ~40% of the planned US$1.3B project cost, this project will capture 500,000 tCO2/year starting in 2025. Thanks to the generous 45Q credit in the IRA, DAC facilities are becoming economical to build. This announcement comes after Oxy purchased Carbon Engineering this year for US$1.1B. The climactic reality of this project is that the planned DAC will be used for enhanced oil recover, creating carbon neutral extraction, so in reality, not changing the balance of carbon in the atmosphere, what’s the point?

- A super interesting branch of technologies that I have been following closely is that of grid-enhancing technologies or GETs. The technologies consisting of advanced power flow control, dynamic line rating, and topology optimization, are all technologies that can unlock transmission capacity and save money for customers at a low investment cost. FERC recognized their importance on Monday and this is hopeful news as ideally the regulation of for-profit utilities to invest in less expensive transmission options like GETs will free up capacity on the grid.