Weekly Climate Recap: Utilities, Transmission, Climate Tech

This was a thrilling week for climate news with a lot of extremely interesting reports and news. In fact, there were several stories that I wanted to touch on but simply didn’t have the space to discuss. Anyway, here is what I found most interesting starting off with a report from the Sierra Club stating the fact that slow moving utilities are in fact, moving slowly in decarbonization efforts. Secondly, and most importantly this week, the IEA has released their report on grids, highlighting that there are a lot of big investments needed to enable the energy transition. Finally, the fourth annual State of Climate Tech report was released by PwC that delves into innovation funding trends within climate tech.

🔌 Utilities are not Moving Fast Enough

Utilities are not moving fast enough on their announced climate goals is the headline from a new report published by the Sierra Club. The Sierra Club is a grassroots environmental organization whose mission is to encourage protection and responsible use of the earth’s ecosystems and resources. The report evaluated the plans of 77 utility companies that are owned by the 50 parent companies that are most invested in coal and gas to examine if they are preparing for the energy transition. These utilities were evaluated based on:

- Plans to retire existing coal generation

- Plans to build new gas capacity

- Plans t build new wind and solar generation

The headline takeaway from this analysis, is not great. Collectively, companies scored 26 points, only up 5 points from the 2022 analysis. The report found that 44 (57%) utilities improved, 9 (12%) made no progress, and 24 worsened (31%). The utilities have plans to retire 35% of coal capacity by 2030 which stands in direct opposition to the IEA declaring that advanced economies must retire all unabated coal. This decision to keep coal online comes as it has been calculated that 99% of all coal plants are more expensive to run than to replace with new solar. To be clear, it is more expensive to just run a coal plant than to build AND run new solar.

This economics of generation also applies to natural gas when you factor in the impact of the Inflation Reduction Act. Despite this, utilities are planning to build an astounding 53 GW of new gas capacity through 2030. An increase of 15 GW versus what was planned to be built in 2022. On the slightly bright side, utilities are proposing the construction of 386 million MWh of clean energy to come online through 2030, but this actually only represents enough capacity to replace 30% of coal and gas generation.

The slow action of utilities can partially be attributed to the regulated nature of the industry. Many utilities earn a fixed rate of return on the money that they invest in projects and the costs are passed down to the consumer of the energy, you and me. Utilities are very risk averse entities as well, as they face penalties for failure to meet demand or preemptively shutting down generation capacity.

Takeaway: While 42 companies of the 50 parent organizations studied reported a climate pledge, it is clear that the vast majority of these pledges represent a kind of greenwashing. Utilities are still taking the sluggish approach to adapting to the clean energy transition. By planning further investment in fossil fuel generation capacity and failure to accept the gravity of the situation, utilities are wasting precious time in the fight against climate change.

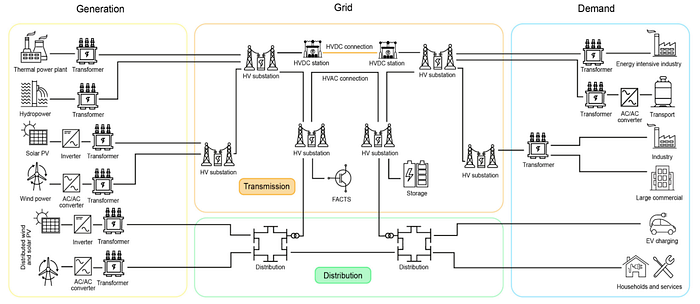

⚡ New IEA Report on Electricity Grids

The IEA has released a new report this week titled “Electricity Grids and Secure Energy Transitions” that dives into the grid requirements to enable the clean energy transition. The report highlights several key areas of insight:

1.Modern, smart and expanded grids are essential for successful energy transitions

- Grids are becoming increasingly important as the clean energy transition progresses but receive far too little attention

- To achieve energy and climate goals, the growth of electricity needs to be 20% faster in the next decade than it was in the previous decade and expanded grids are required to hit these targets

- We need to refurbish or add a total of over 80 million km of grid by 2040 which is the equivalent of the entire existing global grid

- Power systems need to become more flexible as the share of VREs on the grid grows, this includes a bidirectional approach to the grid to leverage distributed resources

2. Grids risk becoming the weak link of clean energy transitions

- At least 3000 GW of renewable energy projects (1500 GW of which is in advanced stages) are waiting in grid connection queues, this is equal to 5 times the amount of solar and wind added in 2022

- Delays in grid investment will slow the energy transition and put 1.5 °C out of reach

- Failure to build out grids will increase reliance on gas, especially relevant given the fragile natural gas markets and concerns about supply

3. Action today can secure grids for the future

- Regulations surrounding the grid need to be reviewed and updated to incentivize grids to keep pace with the changes in electricity demand

- Planning the grid needs to be aligned with planning long term infrastructure investments given the fact that transmission infrastructure takes 5–15 years compared to renewables at 1–5 years

- Grid investment needs to double by 2030 and reach over US$600B per year, especially important as emerging and developing economies have seen declines in grid investment (excluding China)

- Bottlenecks to developing the grid including the supply chain and the workforce need to be addressed through government intervention to create firm and transparent project pipelines

- Barriers to grid development vary by geography such as access to finance in emerging markets and developing economies while regulatory and public acceptance create challenges for advanced economies

Takeaway: In my opinion, the grid is one of, if not the most difficult challenges to overcome in the energy transition. This report from the IEA solidifies my thoughts on the subject. The one statistic alone, 80 million km of new or refurbished grid is a ludicrous figure, for reference, the distance from the Sun to the Earth is about 150 million km. There is a massive uptick in investment in the grid required to enable the transition to the tune of US$600B per year, but it is not just a question of financing, it is a question of timing as well. The biggest challenge within transmission planning is the regulatory front, particularly in advanced economies. The unfortunate reality is that the transmission lines that would be most impactful, are often the hardest to get built due to a variety of constraints.

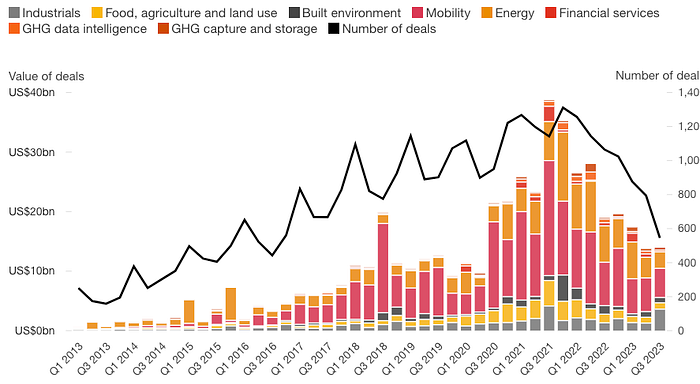

💸 PwC Report Dives into Climate Tech Funding

A new report from PwC, the fourth Annual State of Climate Tech report finds that climate tech investors are expanding their search for companies with growth potential and climate impact. PwC highlights that over the past 2 years, climate investors have had to face a combination of geopolitical turmoil, sinking valuations, inflation, and rising interest rates that all are major headwinds to further investment in climate technologies. The culmination of these factors led to equity and grant funding in climate tech start-ups falling 40.5% yoy vs 50.2% yoy for the broader venture and private equity markets. This drop is especially concerning as the IEA finds that 1/3 in emissions reductions occurring in 2050 relies on technology currently in development as I have previously highlighted.

The report identifies several key trends in the climate-tech space:

A funding shortfall for high-impact climate solutions

- There is a pattern in climate tech company funding, relatively little investment goes into the sectors that generate the most emissions

- However, this trend appears to be changing with capital directed towards industrial emissions (which account for 34% of global emissions) accounting for 8% of funding from Q1 2013 to Q3 2022 vs an increased 14% from Q4 2022 to Q3 2023

- Declining innovation investment in certain technologies reflects the growing maturity of these technologies and commercialization such as solar and wind that are now proven assets

New regional variations

- Climate tech funding in the North American market fell in 2022 compared to 2021 as investors branch out to other regions other than the United States

- When looking at climate tech category by location we see some interesting trends such as a shift away from mobility related start-ups in North America and towards more emissions intensive sectors

Fewer early stage deals, but a steady inflow of first-time investors

- There exists an ongoing slowdown in early-stage dealmaking which may give fewer start-ups the innovation capital needed to succeed thereby reducing availability of viable innovations

- The first reason is investor judgement and the perspective that the technology is not scalable, the second reason is that the overall weakened market makes it difficult for start-ups to raise funds

- Despite the challenges, there is resilience int he form of a steady inflow of first-time funders as new investors per quarter in 2023 has remains relatively steady

How Climate Tech Investors Approach the Changing Market

- Thinking outside the hype in the sense that these climate tech companies must have a fundamental business model, relying on government subsidies is not a reliable business model

- Making countercyclical moves given that the market has come down, the present represents opportunity for investment and created a buyers market

- Plan for growth and understand the dynamics and work required to scale an initial innovation idea to a full fledged company

Takeaway: PwC finds several key trends that are critical to unlocking the final 1/3 of emissions reductions required by 2050 to achieve our decarbonization goals. This report is particularly interesting to me as it represents the pipeline of opportunities that will get us to the state of technology required to decarbonize. Having a strong pipeline of these potential technologies is incredibly important and understanding where the funding is going in the private equity / venture space is critical to forecast where we land on these new and innovative companies that need to scale.

What Else is in the News

- Energy Vault is transitioning from a long duration energy storage company to what I view as an “energy storage solution provider”. Energy Vault was conceived with the idea of stacking blocks by crane in what would be the storage of potential energy. Then lowering the blocks to generate electricity. However, in an interesting read from Canary Media, it is highlighted that Energy Vault is transitioning to multiple energy storage tools such as batteries, hydrogen, and their gravitational storage solution. This transition represents the dominance of batteries in the vast majority of applications that are needed on the grid and a company realizing that their solution is not a silver bullet for all energy storage applications.

- A new analysis from Resources for the Future finds dives deep into the economic benefits of achieving the Paris Agreement Goals. Using detailed, probabilistic representations of uncertainty in future socioeconomic, emissions, and temperature trajectories and the impact on our society in terms of mortality, agricultural losses, energy use, and coast effects, the analysis produces some incredible figures. Mitigation efforts aimed at reducing global warming from a 2.5°C temperature increase to below 2°C would yield an estimated $467 trillion in cumulative economic benefits by 2300, equivalent to 1.5% of the expected present value of global GDP over the same period. In annual terms, this amounts to $5.2 trillion. If the temperature increase is further limited to below 1.5°C, an additional $138 trillion in benefits would be realized, resulting in a total benefit of $605 trillion or 2% of cumulative GDP, which equates to $6.8 trillion annually.

- Fossil fuel markets are frothy on the back of conflict in the Middle East. As the conflict unfolds between Hamas and Israel, the price of Brent continues to swing. Further news in the Middle East as Shell has decided to purchase LNG from Qatar for 27 years as reported by Bloomberg. This deal will supply the Netherlands with supply of fossil fuels despite increasingly ambitious claims by the EU to decarbonize. This deal marks Qatars second major deal to supply fossil fuels to the EU Bloc.